")

- Navigation image")

Read “The Global State of Commerce 2026” report

He was a serial abuser, dodging first-party fraud detection while buying thousands of dollars’ worth of merchandise from multiple online retailers with his own credit card — only to claim he never received his packages. When questioned, he successfully double-talked his way through the evidence. But he met his match: cutting-edge, first-party fraud detection that relies on a global data network to understand the identity and intent behind ecommerce transactions. The fresh insights shut him down.“It’s not something one merchant can do easily,” says Signifyd’s Senior Director, Risk Operations Tara Mitchell. But with the right tools and strategies, every ecommerce platform can keep its customers happy and protect its bottom line.

Key Takeaways

- What is First-Party Fraud? It involves a customer using their own genuine identity (real name/credit card) to defraud a retailer, typically through various types of chargeback abuse (e.g., falsely claiming “Item Not Received” or “Item Not As Described”).

- Widespread and Costly: This fraud is on the rise (up 8% in H1 2025) and costs U.S. merchants billions annually. As many as one in five consumers admit to committing this type of fraud or abuse.

- Why It’s Hard to Detect: Unlike traditional fraud, the rightful cardholder is involved, making intent difficult to prove. Overly strict rules risk alienating good customers who may accidentally file a chargeback.

- Traditional Methods Fail: Manually fighting chargebacks has a low win rate (17%). Effective solutions require moving beyond internal data checks and manual reviews.

- The Solution is Network-Based AI: The most effective defense uses AI and machine learning across a large, global data network to analyze transactions in real-time and uncover the true intent behind the purchase, dispute, or return.

What is first-party fraud?

First-party fraud is any type of fraud that involves using a real, genuine identity to defraud an ecommerce company. This could be various types of chargeback fraud, including a customer falsely claiming they did not receive an item or falsely claiming that an item was not satisfactory or damaged. The idea being to keep the item and receive a replacement or refund.

In some cases, first-party fraud is carefully planned; the culprits may be operating as individuals or part of a large organized ring. In other cases, it’s opportunistic, or even accidental. A customer with a clean record may take advantage of a lenient return policy, or fail to recognize a credit card transaction and report it as fraud.

Seven types of ecommerce first-party fraud

First-party fraud (also known as friendly fraud or first-party abuse) used to primarily refer to any fraud committed by the rightful credit card holder at checkout. But as fraudsters’ techniques have become more sophisticated and consumers’ actions have become more brazen, the definition has expanded to include the following:

- Item not received (INR): Someone orders a product online and falsely claims it was not received, intending to pocket the refund and keep (or resell) the item.

- Item significantly not as described (SNAD): Once a product arrives, a customer falsely claims it was different from the description, damaged or defective to get a refund.

- Chargeback abuse: A customer intentionally purchases something with their credit card, then requests a chargeback from the credit-card merchant, claiming the charge was fraudulent.

- Promo abuse: A customer takes advantage of a free trial or another type of promotion by signing up for multiple accounts using different email addresses. They may also create multiple accounts in the hopes of securing referral bonuses.

- Unauthorized reselling: A fraudster or fraud ring seeks to corner the market for a desirable and/or scarce product with a plan to resell it at a considerable profit. The maneuver leaves legitimate customers frustrated and often angry with the original retailer. After securing a product through fraudulent means, the fraudster goes on to resell the product

- Wardrobing: A form of return abuse where a customer takes advantage of a lenient return policy and returns an item for a full refund after wearing it just once or a few times, often to an event.

- Bracketing: Someone purchases multiple versions of the same product, intending to keep only one and return the rest.

Ultimately, first-party fraud now commonly refers to almost any type of fraud other than traditional payment fraud, where stolen or falsified information is used to commit fraud.

How does first-party fraud impact ecommerce businesses?

First-party fraud leads to significant financial losses to ecommerce businesses. While fraudsters may view first-party fraud as a victimless crime, when unchecked, it costs businesses substantially and drives up prices for every consumer.

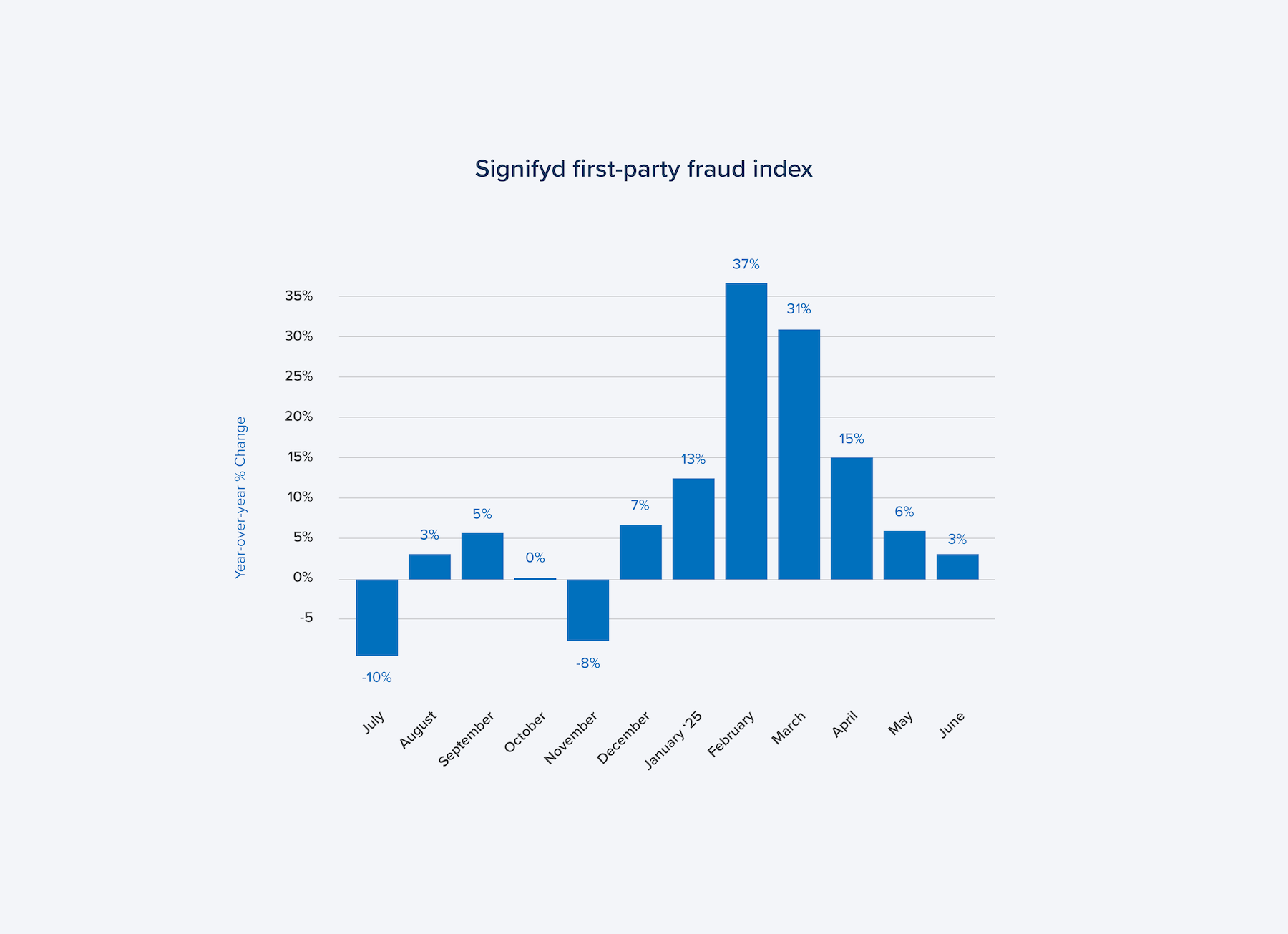

Source: Signifyd data

Signifyd data shows that first-party fraud was up by 8% in the first half of 2025 compared to 2024. And polling conducted for Signifyd shows that as many as one in five consumer admit to having committed first-party fraud.

Common challenges of first-party fraud

The challenges of first-party fraud are wide-ranging. What first appears to be first-party fraud may, on closer inspection, turn out to be a genuine transaction, and vice versa.

Retailers know an overzealous fraud prevention strategy can lead to alienating genuine customers. On the other hand, word of a lax approach to first-party fraud can spread quickly, making your business a target.

Customer experience

Many ecommerce platforms employ a customer-first approach to payment processing and returns, for good reason: Shoppers whose orders are falsely declined spend nearly 16% less on subsequent orders.

In some cases, a less-than-perfect customer experience may be an incentive for an otherwise good customer to commit first-party fraud.

Accidental fraud

It’s not unusual for customers to review their credit card statement, not recognize a purchase they made, and report it in the form of a chargeback as fraud. The business still loses money, but the customer didn’t knowingly defraud them. By its nature, accidental friendly fraud is all but impossible to predict.

“I’ve looked at my credit card statement and not recognized a transaction,” says Mitchell. “Instead of it showing the name of a coffee shop, it shows the name of the parent company. If I didn’t spend time thinking about it, I would assume it was a fraudulent charge.”

Developing fraud techniques

As fraud detection becomes more sophisticated, so do the methods and technology employed by fraud rings. Financial information may be manipulated, or culprits may learn to imitate legitimate transactions to evade detection. Retailers must stay one step ahead.

Data integration and accessibility

Accessing, compiling and reviewing the data necessary for establishing intent (the key to catching first-party fraud) is no small task for internal fraud prevention teams.

Cost

It’s a double hit for ecommerce platforms: If a company gives a refund and the customer keeps the product, the value is lost twice over. First-party fraud, such as INR and SNAD, costs U.S. merchants $50 billion a year, according to Mastercard. Moreover, research from the Merchant Risk Council shows that merchants report spending $35 for every $100 in first-party disputes to manage the challenge.

Company culture

As ecommerce expands, fraudsters refine their tactics — a lenient approach to first-party fraud costs more than it used to. Retailers must shift company culture from the top down to reflect this new reality.

Strategies to combat first-party fraud

Without a proper strategy or the aid of a commerce protection partner, merchants often scramble to find strategies to navigate the muddle of INR and SNAD claims.

While many merchants report disputing chargebacks to fight first-party fraud, according to the 2025 Merchant Risk Council’s ecommerce and fraud report, the overall win rate is only 17%. Instead, merchants reported that the following strategies were more effective for combating first-party fraud:

- Detailed credit card descriptors: Better credit card descriptors on consumers’ bills help combat accidental fraud claims.

- Review genuine chargebacks and refunds: Analyzing non-fraud chargebacks and declines alert merchants to suspicious transactions.

- Monitor transaction data: Reviewing and analyzing transaction data for unusual activities or anomalies helps identify culprits.

- Require a signature on delivery: Decreases the chance of fraudulent INR incidents but adds friction to the buying process.

Online brands should carefully review any changes made to their process to ensure they’re not inconveniencing customers. A lack of precision leads to false positives, rejecting revenue and alienating potential customers.

How to prevent fraud by using machine-learning fraud detection?

Without the aid of a commerce protection provider, merchants struggle to separate the signal from the noise. Ecommerce platforms should shift their mindset from internal-only data checks to a more refined, comprehensive approach to first-party fraud, including:

AI and machine learning

Signifyd’s Decision Center pulls INR and SNAD abuse data in real-time, giving customer support teams the ability to apply appropriate automated responses to disputes and returns requests.

These types of continuously improving tools can detect patterns that humans, or rules-based systems, overlook. With Signifyd, “Every case gets investigated,” Mitchell says. Refunds and disputes are run through machine learning models that assess them for evidence of friendly fraud.

Network analysis and reporting

Advanced network analysis examines interactions and relationships across:

- Devices

- Accounts

- IP addresses

Advanced reporting across enriched data uncovers the intent behind a transaction, which can be an incredibly difficult task for internal teams to manage at scale.

Advanced anomaly detection

Sudden changes in purchasing behavior, such as the number or value of purchases made by an individual, can be warning signs of first-party or third-party fraud.

Machine learning tools can review such anomalies in real-time and retrospectively — a powerful combination for short and long-term fraud prevention.

Integrated data environments

Larger data ecosystems lead to more accurate results. With access to internal and external databases and over 600 million digital wallets, Signifyd paints a detailed picture of a purchaser’s history and risk of criminal intent.

Real-time analysis

By analyzing transactions in real-time, ecommerce platforms can screen out first-party fraud on the front end and retain their customer-friendly return policies. Signifyd’s Commerce Protection Platform automates fraud protection by approving or declining transactions in real-time.

Transaction monitoring

Advanced detection algorithms can detect unusual velocity, such as a high number of transactions in a short period (a common indicator of fraudulent activity). Signifyd’s machine learning models detect unusually fast series of transactions in real time, cutting off fraudsters in their tracks.

Leveraging purpose-built first-party fraud detection

First-party fraud isn’t easy to detect. But every crime leaves clues, and Signifyd provides the tools every ecommerce retailer needs to uncover them—including Complete Chargeback Protection, Intelligent Returns for greater insights into return intent, and Return Abuse Prevention.

With a combination of advanced AI solutions and human expertise, retailers can keep customers happy, their bottom line healthy and fraudsters at bay.

Frequently Asked Questions

Who commits first-party fraud?

When it comes to first-party fraud, there is no one archetype. People committing first-party fraud may be:

- Individual consumers: They may commit fraud as a one-off or more than once after discovering loopholes or weaknesses in a system. They may be financially hard-up, opportunistic or don’t believe their actions will have consequences.

- Fraud rings: A network of individuals intent on profiting from fraud and abuse. They may use sophisticated technology to evade detection, or know the right things to say if they’re caught. Criminal rings also establish “fraud as a service” operations, offering to commit fraud on behalf of consumers looking to take advantage.

- Why is first-party fraud hard to detect?

First-party fraud is difficult to detect because the transactions are generally conducted by the rightful credit card owner. First-party fraud and abuse can also occur at several different sites along the buying journey. It is best detected by relying on a large data network that provides reliable insights beyond what an individual merchant’s data can provide

What’s the difference between first and third-party fraud?

In first-party fraud, the fraudster generally uses their own identity. It can surface at checkout or in the fulfillment and post-delivery stages in the case of illegitimate disputes and return fraud and abuse. Third-party fraud generally occurs at checkout and involves stolen credentials or synthetic identities.

What are the most effective prevention strategies for first-party fraud?

Human intelligence paired with AI and machine learning tools is the best way to prevent first-party fraud.

Signifyd provides advanced machine learning models, pattern recognition and real-time transaction monitoring to provide an understanding of identity and intent behind every transaction, all backed by leading data scientists and fraud and risk specialists. Internal strategies, such as manual data monitoring and requesting a signature on delivery, can also help prevent some forms of first-party fraud.

Signifyd blog authors Maryann Hudson and Justin Fogarty contributed to this report.

Want to learn more about tackling first-party fraud? Let’s talk.