")

- Navigation image")

Read “The State of Fraud 2023” report

The painful truth is that ecommerce merchants need a chargeback guarantee more than ever.

A chargeback in online retail amounts to an un-conversion. A transaction that was a sale suddenly isn’t anymore. Not only that, but a chargeback transforms a money-making event into a cost to the business. It’s no wonder then that merchants are constantly looking for the best way to avoid chargebacks — and when that isn’t possible the best way to eliminate the cost of chargebacks to the business.

In 2023, the surest way to accomplish both of those things is through fraud protection for merchants that offers a chargeback guarantee.

What is a chargeback guarantee?

A chargeback guarantee is a contractual promise from a fraud protection vendor that it will reimburse a merchant for an approved order that turns out to be fraudulent. One important factor to note is that different fraud protection providers add different conditions to their chargeback guarantees, which in some cases limit the protection a merchant enjoys with a given provider.And many providers don’t offer a guarantee at all.To better understand the concept of a chargeback guarantee, it’s important to understand what a chargeback is and how they originate. The most commonly discussed chargebacks occur when an unauthorized charge is made on a consumer’s credit card. Such charges are generally the result of criminal activity. Fraud rings, for instance, use stolen credentials available for purchase on the Dark Web to make online purchases for which they’ll never be billed.

Who pays for a chargeback?

The legitimate cardholder in such cases is billed for the fraudulent order and that’s when the consumer takes corrective action. Often that action is to bypass the merchant and directly contact the bank that issued their credit card to report the fraudulent order. At that point, the bank issues a chargeback — essentially a refund on behalf of the merchant. The bank then requires the merchant to reimburse the bank for the payment it made to the consumer. In such cases, both the merchant and the consumer are victims, but only the merchant is responsible for making things right. The chargeback process and response is unique to online orders — known as card-not-present transactions. When a credit card is used fraudulently in a store — a card-present transaction — the card issuing bank takes on the liability for the fraudulent activity. That’s not the case for an online order.

At that point, the bank issues a chargeback — essentially a refund on behalf of the merchant. The bank then requires the merchant to reimburse the bank for the payment it made to the consumer. In such cases, both the merchant and the consumer are victims, but only the merchant is responsible for making things right. The chargeback process and response is unique to online orders — known as card-not-present transactions. When a credit card is used fraudulently in a store — a card-present transaction — the card issuing bank takes on the liability for the fraudulent activity. That’s not the case for an online order.

Are there other types of chargebacks

While orders made with stolen credit cards or credentials are among the most common chargebacks, chargebacks come about in a variety of ways. Consumers will sometimes request a chargeback from their card-issuing banks because of a dispute or mishap involving a merchant or a delivery company. For instance, a consumer might request a chargeback for a package that never arrives — a circumstance known as “item not received” or INR. Or a customer might be disappointed in a product that arrives, arguing it is different or lesser than what was described on the website. Or a product might arrive damaged or missing parts or pieces. In those cases, the term used is “significantly not as described” or SNAD. Chargebacks fraud can also result from cases of “first-party” fraud (sometimes called “friendly fraud”) — or cases in which the legitimate cardholder claims they did not charge an item they did charge. Other times a member of the cardholder’s household or family charged an item without the knowledge or permission of the cardholder, which leads to a chargeback.

Chargebacks fraud can also result from cases of “first-party” fraud (sometimes called “friendly fraud”) — or cases in which the legitimate cardholder claims they did not charge an item they did charge. Other times a member of the cardholder’s household or family charged an item without the knowledge or permission of the cardholder, which leads to a chargeback.

Who decides a chargeback is warranted?

In those cases, some consumers will go straight to their bank and request a chargeback rather than contact the merchant in an effort to receive a satisfactory outcome. These claims — and claims regarding fraudulent orders — can become tricky when it isn’t clear whether the legitimate cardholder is being truthful. The responsibility for proving a chargeback is not warranted falls to the merchant — and to any third-party provider they might work with to mitigate fraud and/or to manage chargebacks.

How big of a problem are chargebacks in ecommerce?

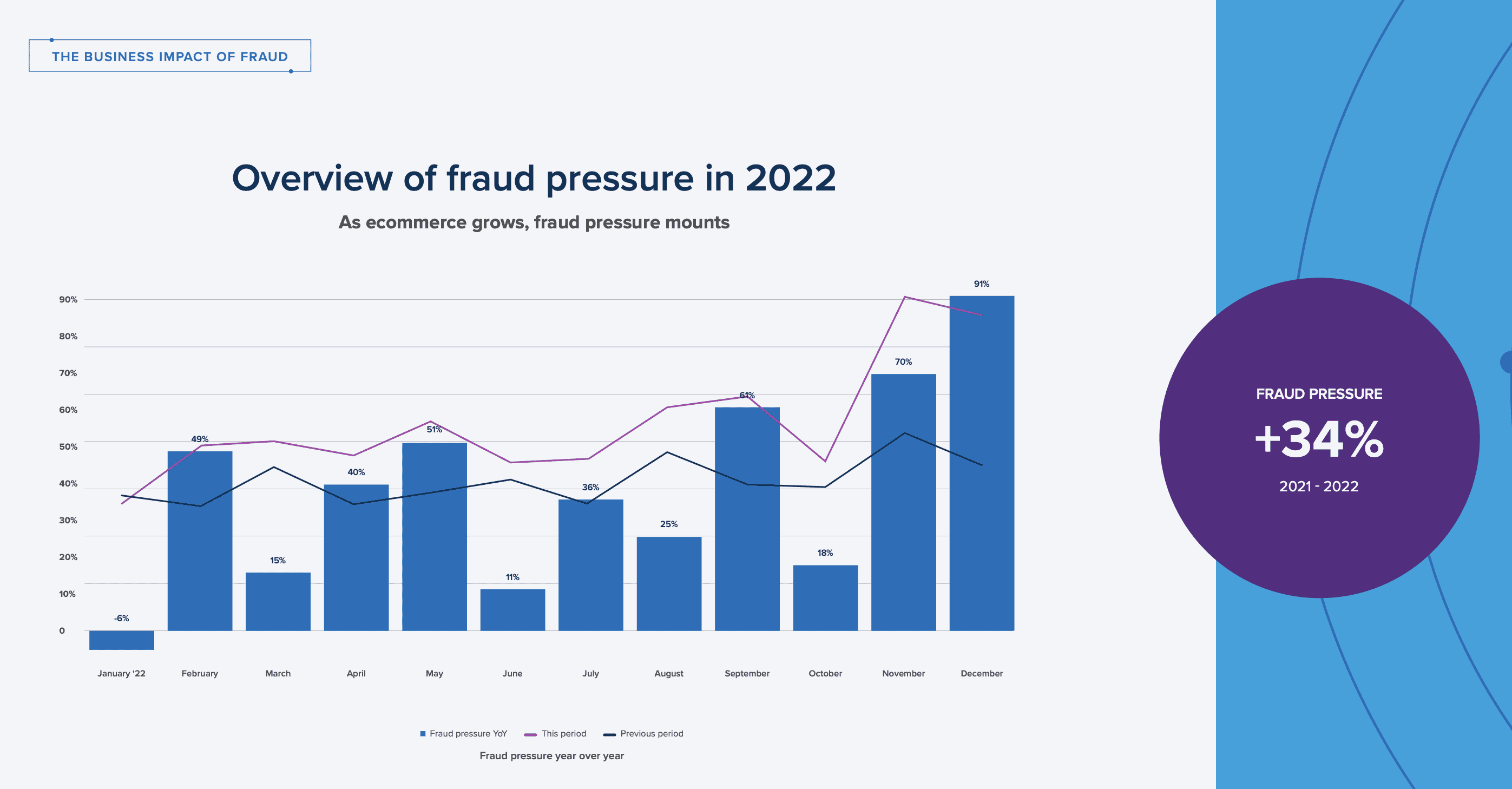

Chargebacks are a bigger problem than they were a year ago, which was a bigger problem than the year before that — and so on. As ecommerce becomes a bigger portion of retail sales, online fraud becomes a bigger — and more expensive — problem. Both the volume of fraud and the cost of each individual fraudulent order are on the rise.Fraud pressure — or the increase in presumably fraudulent orders on Signifyd’s Commerce Network — rose 34% in 2022, according to Signifyd data reported in “The State of Fraud 2023.”

And the total cost of fraud — which includes things like shipping and fulfillment costs, chargeback fees, sales taxes, etc. — rose nearly 6% in 2022, increasing from $196 for every $100 in fraudulent orders to $207 for every $100 in fraudulent orders.

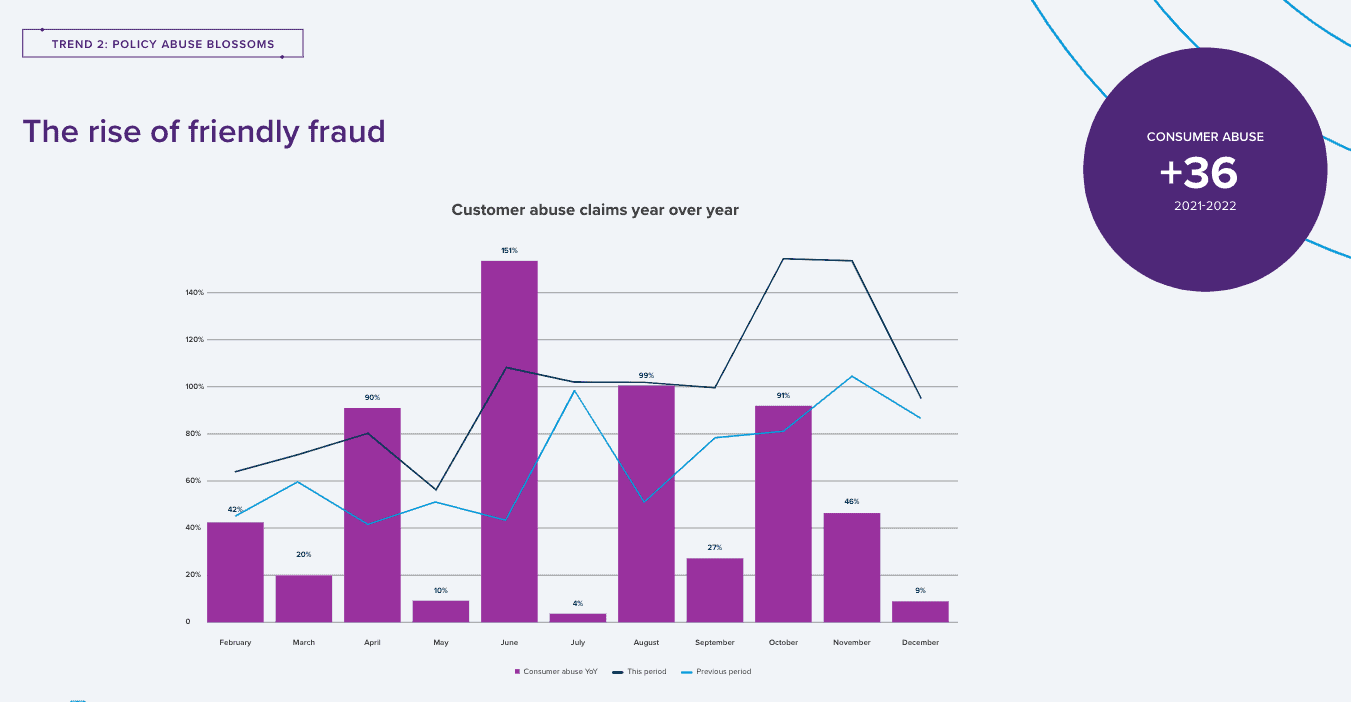

Furthermore, first-party fraud is also on the rise — outpacing the growth in traditional payment fraud. The type of fraud that includes false complaints about items not received or goods received in poor condition was up 36% in 2022.

Does a guarantee cover more than the cost of goods?

Again, different fraud prevention companies provide different levels of coverage. Some cover not only the cost of lost goods, but also shipping fees, sales taxes, chargeback fees and related costs. Many, however, don’t provide any financial guarantee. Some limit the goods a guarantee applies to and some limit the size of loss they will cover. Some providers guarantee some types of chargebacks, but not others — they might not cover chargebacks related to first-party fraud for instance.

Are all chargeback guarantee solutions the same?

It’s important to research, ask questions and fully understand just what is covered by any provider you’re considering. Signifyd, for instance, is the only provider that offers a guarantee on all manner of chargebacks – both fraud chargebacks and non-fraud chargebacks. It’s also important to understand just what costs the chargeback guarantee covers. Is it just the cost of the product? Signifyd’s guarantee provides reimbursement for the product and associated costs, including the chargeback amount, shipping fees and associated processor fees. The best chargeback coverage also manages the chargeback process for the merchant. Contesting a chargeback involves a quasi-judicial process that relies on documentation and other evidence to determine whether the chargeback is legitimate or not.

The best chargeback coverage also manages the chargeback process for the merchant. Contesting a chargeback involves a quasi-judicial process that relies on documentation and other evidence to determine whether the chargeback is legitimate or not.

How did the chargeback guarantee come about?

Chargeback guarantees were first offered by a few pioneering fraud protection providers, including Signifyd, beginning in the 2010s. Signifyd co-founders Raj Ramanand and Mike Liberty, for instance, both worked in risk intelligence at PayPal.

Signifyd CEO Raj Ramanand

They were rankled by the fact that when credit card fraud was committed in a store, the issuing bank took on the liability for the loss, but when credit card fraud was committed online, the merchant took the loss.

The bifurcated system seemed inherently unfair and they sought to find a way to relieve the financial burden of fraud from online retailers and brands. They came up with the concept of guaranteed fraud protection, in essence, a chargeback guarantee.

How does a chargeback guarantee work?

As we said, a chargeback guarantee is pretty much what it sounds like. But there is a little more to it. First of all, in order to offer a financial guarantee for approved orders that turn out to be fraudulent, a provider must be supremely confident in its decisions. And on the merchant’s side, a brand must have strong reassurance that a fraud protection provider isn’t going to be meek and turn down any order arriving with red flags simply to avoid having to pay the merchant for the cost of fraud. Mistakenly declining an order for fear of fraud — a false decline, in other words — is a merchant’s worst enemy.  Merchants relying on legacy fraud prevention systems, whether they depend largely on manual review or heavily on static, rules-based systems — can lose more money due to false declines than they do to fraudulent orders. The loss of revenue spirals when you consider the insult rate — a certain percentage of customers whose legitimate orders are turned down will refuse to shop again with the merchant who improperly rejected their business.

Merchants relying on legacy fraud prevention systems, whether they depend largely on manual review or heavily on static, rules-based systems — can lose more money due to false declines than they do to fraudulent orders. The loss of revenue spirals when you consider the insult rate — a certain percentage of customers whose legitimate orders are turned down will refuse to shop again with the merchant who improperly rejected their business.

How can a fraud protection vendor afford to guarantee decisions?

Fraud protection with a chargeback guarantee is typically structured to align the financial interests of the merchant and the provider. Signifyd, for instance, only charges for orders it approves. If it doesn’t approve an order, it doesn’t receive any fee. Therefore, it’s in the best interest of both the merchant and Signifyd to ship every legitimate order, so as not to turn away customers who are willing to pay for what the merchant is selling. But that revenue model doesn’t work for every fraud protection provider. Some have recently moved away from guarantees and adopted a “best effort” model after initially providing chargeback guarantees. Poor decisioning can be extremely costly and result in a business model that is not sustainable.

If not guaranteed fraud protection, then what?

The retreat has given rise to performance service level agreements (performance SLAs or performance guarantees) and a sales narrative that pits performance SLAs against chargeback guarantees. Performance SLAs promise a certain level of performance around metrics such as approval rates, chargeback rate and fulfillment time. Unlike chargeback guarantees, performance SLAs don’t include a financial guaranteeThe downside to performance SLAs lies in the options available to a fraud prevention provider to meet them. One way to meet chargeback guarantees is to become more conservative and decline more orders to make sure they are not later subject to chargebacks. This leads to false declines or false positives.Or consider the need to meet a certain approval rate. What happens when the merchant is the victim of a fraud attack? Online merchants can see dramatic waves of fraudulent orders when they are under attack. A performance SLA provider would have a hard time meeting an approval rate SLA when a significant percentage of incoming orders are fraudulent. The temptation would be to approve the orders to meet the promised level of approvals.

What does it take to be a successful guarantee provider?

Building a successful chargeback guarantee business requires vast amounts of transaction intelligence and superior machine learning models. Without those two things, a provider would find itself paying too much and too often for fraudulent orders that evade their automated systems.  Signifyd, for instance, makes its ship-or-don’t-ship decisions based on a global Commerce Network of thousands of merchants accepting millions of transactions from hundreds of millions of consumers. Its Commerce Protection Platform consists of powerful machine-learning models that instantly sort fraudulent orders from valid ones, ensuring that legitimate customers are not frustrated by being incorrectly declined when they click the buy button. In fact, Signifyd has seen elements elsewhere on its network included in 98% of the orders placed with any given merchant on its network. In essence, Signifyd can offer a chargeback guarantee because it understands the identity and intent behind each transaction.

Signifyd, for instance, makes its ship-or-don’t-ship decisions based on a global Commerce Network of thousands of merchants accepting millions of transactions from hundreds of millions of consumers. Its Commerce Protection Platform consists of powerful machine-learning models that instantly sort fraudulent orders from valid ones, ensuring that legitimate customers are not frustrated by being incorrectly declined when they click the buy button. In fact, Signifyd has seen elements elsewhere on its network included in 98% of the orders placed with any given merchant on its network. In essence, Signifyd can offer a chargeback guarantee because it understands the identity and intent behind each transaction.

The story of chargeback guarantees in ecommerce

The notion of fraud protection with a chargeback guarantee came about to address the inequity of who is liable for a loss when a criminal or wayward consumer takes advantage of an online merchant versus a merchant selling in a physical store. Rather than saddle an online merchant with the loss when a fraudster makes off with a product, a chargeback guarantee means the fraud protection provider will make the merchant whole — provided that it has approved the order as legitimate. The best in the business extend the chargeback guarantee beyond payment fraud to first-party fraud — cases in which the rightful cardholder takes advantage.

There is more than one kind of chargeback

First-party fraud or abuse can take the form of false claims that a package never arrived or that the product was damaged or otherwise not as described by the merchant. The best coverage also manages those chargebacks for a merchant, handling the requirements for paperwork and essentially building a case. The chargeback guarantee model aligns the interests of the merchant and the fraud protection provider. The provider is only paid for orders it approves, meaning that to optimize revenue, both parties want to make sure every legitimate order gets shipped. For those reasons, a chargeback guarantee model won’t work for every fraud protection provider. Some have backed away from the model recently, as achieving success requires a vast network that produces voluminous amounts of transaction intelligence and machine-learning models that can keep up with an increasingly diabolical community of fraud rings.

Why a chargeback guarantee model is valuable for online merchants

Despite the difficulty in providing a chargeback guarantee, the assurance from a commerce protection provider can be extremely valuable from the merchant’s perspective. Such a guarantee means a merchant can ship orders fearlessly, freeing up time, resources and energy to focus on core aspects of its retail business.The automated nature of most guarantee chargeback models, speeds up orders and dramatically reduces false declines, which means a better customer experience for shoppers on a merchant’s site.And because chargeback guarantee models typically charge a small percentage of approved orders, the model aligns the interests of the fraud-protection provider and the merchant — both want to ship as many orders as possible while avoiding shipping fraudulent orders. That alignment means that the chargeback guarantee model is literally a win-win. Feature photo by Getty Images; additional images by Getting Images and Signifyd

Looking to optimize your revenue with a chargeback guarantee? Let’s talk.